QUOTE OF THE DAY

...beware of incoherence that passes itself off as complexity. Dani Rodrik

RETIREMENT FINANCE AND PLANNING

Are SUVs Ruining Retirement Savings? Ben Carlson

if you’re one of the many people who are woefully unprepared

for retirement or any of your other saving goals, a good place to start would

be cutting back on any unnecessary spending on transportation. http://awealthofcommonsense.com/2018/07/are-suvs-ruining-retirement-savings/

Target-Date Funds Aren’t the Retirement Bull’s-Eye, Nir

Kaissar

target-date funds are no cure-all. One obvious defect is

fees. I counted 227 retirement share class target-date funds with $100 million

or more in net assets. Their average expense ratio is 0.67 percent a year, and

their asset-weighted average expense ratio — which accounts for the size of the

funds — is 0.58 percent…It’s also not clear why retirement savers should own

more bonds over time. People are living longer and a bond-heavy portfolio

raises the risk of running out of money. And that isn’t the only risk…The

combination of those factors — high fees and the potential for unlucky timing

and misuse — could easily add up to 1 percent to 2 percent a year in lower

returns, costing retirement savers hundreds of thousands of dollars over the

course of a career. https://www.bloomberg.com/view/articles/2018-07-18/target-date-funds-aren-t-the-retirement-bull-s-eye

The Unique Retirement Issues Facing Women, Swedroe

Women face at least 12 unique challenges from financial and

life circumstances related to long-term retirement planning. … Specifically,

women: 1. Earn less. 2. Live

longer. 3. Have fewer years of earned

income. 4. Start investing later… https://www.advisorperspectives.com/articles/2018/07/30/the-unique-retirement-issues-facing-women

Why is Retirement Harder than Saving for Retirement? (SWR

Series Part 27), ERN

ust because saving for retirement is relatively simple it

doesn’t mean we can just extrapolate that simplicity to the withdrawals during

retirement. And that’s what today’s post is about: I like to go through some of

the fundamental factors that make withdrawing money more complicated than

saving for retirement. Think of this as an introduction to the SWR Series that

I would have written back then if I had known what I know now! https://earlyretirementnow.com/2018/07/25/why-is-retirement-harder-than-saving-for-retirement-swr-series-part-27/

MARKETS AND INVESTING

The Myth of Volatility Drag (Part 2), Will Morrison

What? Calling it “drag” creates an association since “drag”

is generally understood as a force. But there is no “force” here, merely a

mathematical relationship.

[I find this kind of thing useful. If Mr Morrison does a

part 3 of this series I hope that he goes beyond the useful focus on semantic

issues and the effects of time over multiple periods. I hope he includes a

discussion of both (a) consumption (often ignored) which can introduce a very

real buy-high-sell-low effect into the volatility equation and (b) horizon

(while the tendency at infinity is towards return expectations adjusted by -V/2

it’s a slightly different game between now and infinity, a game retirees play

every day)]

Machine Learning, Subset Resampling, and Portfolio

Optimization, Justin Sibears

building a robust portfolio optimization engine requires a

diligent focus on estimation risk…We summarize the results from two recent

papers we’ve reviewed on the topic of managing estimation risk. The first paper

relies on techniques from machine learning while the second paper uses a form

of simulation called subset resampling….We perform our own tests by building

minimum variance portfolios using the 49 Fama/French industry portfolios. We find that while both outperform

equal-weighting on a risk-adjusted basis, the results are not statistically

significant at the 5% level. https://blog.thinknewfound.com/2018/07/machine-learning-subset-resampling-and-portfolio-optimization/

ALTERNATIVE RISK

Winton’s David Harding on Turning Away From Trend Following,

winton.com

Momentum is not a fixed law of markets, he says; it was a

good trade and it got crowded. “If any trade gets very crowded then it can

backfire,” he says. “It’s a standard market thing. If everyone tries to do the

same thing at the same time it goes wrong.” … Equally he rejects the suggestion

that because trend-following returns have waned, the opportunity for firms like

Winton has shrunk. Such thinking comes from the flawed assumption that markets

fit the efficient market model, he says. … his view of market returns as “in

general the product of a complex, multidimensional chaotic process” impossible

to characterise by any simple mathematical model. … The quant culture in

finance, conversely, he sees as often dogmatic. “Many mathematicians and

programmers don’t read a lot of history, philosophy, religion,” Harding says.

“That’s what you need to be a successful investor. You need to have an eclectic

outlook on the world.” https://www.winton.com/news/2018/risk-net-wintons-david-harding-on-turning-away-from-trend-following

The dangerous disregard for fat tails in quantitative

finance, sr-sv

With fat tail distributions, extreme events away from the

centre of the distribution play a very large role. Black swans are not more

frequent, they are more consequential. The fattest tail distribution has just

one very large extreme deviation, rather than many departures form the norm. http://www.sr-sv.com/the-dangerous-disregard-of-fat-tails-in-quantitative-finance/

Academics Avoid Equity Curves, priceactionlab

Equity curves show the increase in equity of an investment

strategy as a function of time. This is the most valuable data visualization

for people with skin-in-the-game. http://www.priceactionlab.com/Blog/2018/07/equity-curve/

Momentum Solutions for Retirement, dualmomentum.net

But the vast majority of SWR studies are based on various

allocations of buy-and-hold portfolios of stocks and bonds. Researchers have only recently begun to

consider how the SWR calculus could be affected by factor-based investment

styles like value or momentum (Kitces 2016[5] ; Gray 2017[6]). … At least one investor in the momentum camp,

Toma Hentea (2015)[8], compared SWRs of buy-and-hold portfolios to those of

momentum-based portfolios and noted that SWRs could be substantially higher for

momentum-based portfolios. … Many

investors could benefit from incorporating some element of momentum strategies

into managing their retirement accounts, whether to accomplish a higher

withdrawal rate or simply to reap the well-established benefits of momentum and

trend following for other purposes. http://www.dualmomentum.net/2018/07/momentum-solutions-for-retirement.html

Reducing the Risk of Black Swans: Using the Science of

Investing to Capture Returns with Less Volatility (a review), Swedroe and

Grogan

This new edition revamps the previous one by elucidating two

key developments: (1) “the ‘retailization’ of investment strategies that were

once solely the domain of hedge funds and institutional investors such as the

Yale Endowment Fund” and (2) the fintech revolution, which has disintermediated

traditional lenders and, in the process, created new channels of access for a

broader swath of investors. These developments, according to the authors, have

made possible investment vehicles that embody uncorrelated return factors

beyond the Fama–French set. As a result, financial advisers and sophisticated

retail investors can avail themselves of the full menu of style and risk

factors previously accessible only to endowments and other large institutional

investors via private equity, hedge funds, and more-esoteric vehicles. https://www.cfapubs.org/doi/full/10.2469/br.v13.n1.4%40faj.2018.74.issue-2

Everybody’s Doing It: Short Volatility Strategies and Shadow

Financial Insurers, FAJ The extraordinary growth of short volatility strategies

creates risks that may trigger a serious market crash. A low-yield,

low-volatility environment has drawn various market participants into

essentially similar short volatility-contingent strategies with a common

nonlinear risk factor. We discuss these strategies, their commonalities, and

the generally unrecognized risks that they would pose if everyone were to

unwind simultaneously. Volatility-selling investors essentially provide “shadow

financial insurance.” Investors and regulators would benefit from preparing for

large, self-reinforcing technical unwinds that may occur when/if central banks

change policy or macro or political events affect investor confidence. We also discuss

potential mechanisms that might provide stabilization against largely adverse

financial outcomes. https://www.cfapubs.org/doi/pdf/10.2469/faj.v74.n2.6

Measuring Process Diversification in Trend Following, Corey

Hoffstein

In this commentary, we attempt to measure how much

diversification opportunity is available by employing multiple models with

multiple parameterizations in a simple long/flat trend-following process. … As

it specifically pertains to trend-following, we see that diversification

appears to be maximized by allocating across a number of lookback horizons,

with an optimizer putting a particular emphasis on barbelling shorter and

longer lookback periods. https://blog.thinknewfound.com/2018/07/measuring-process-diversification-in-trend-following/

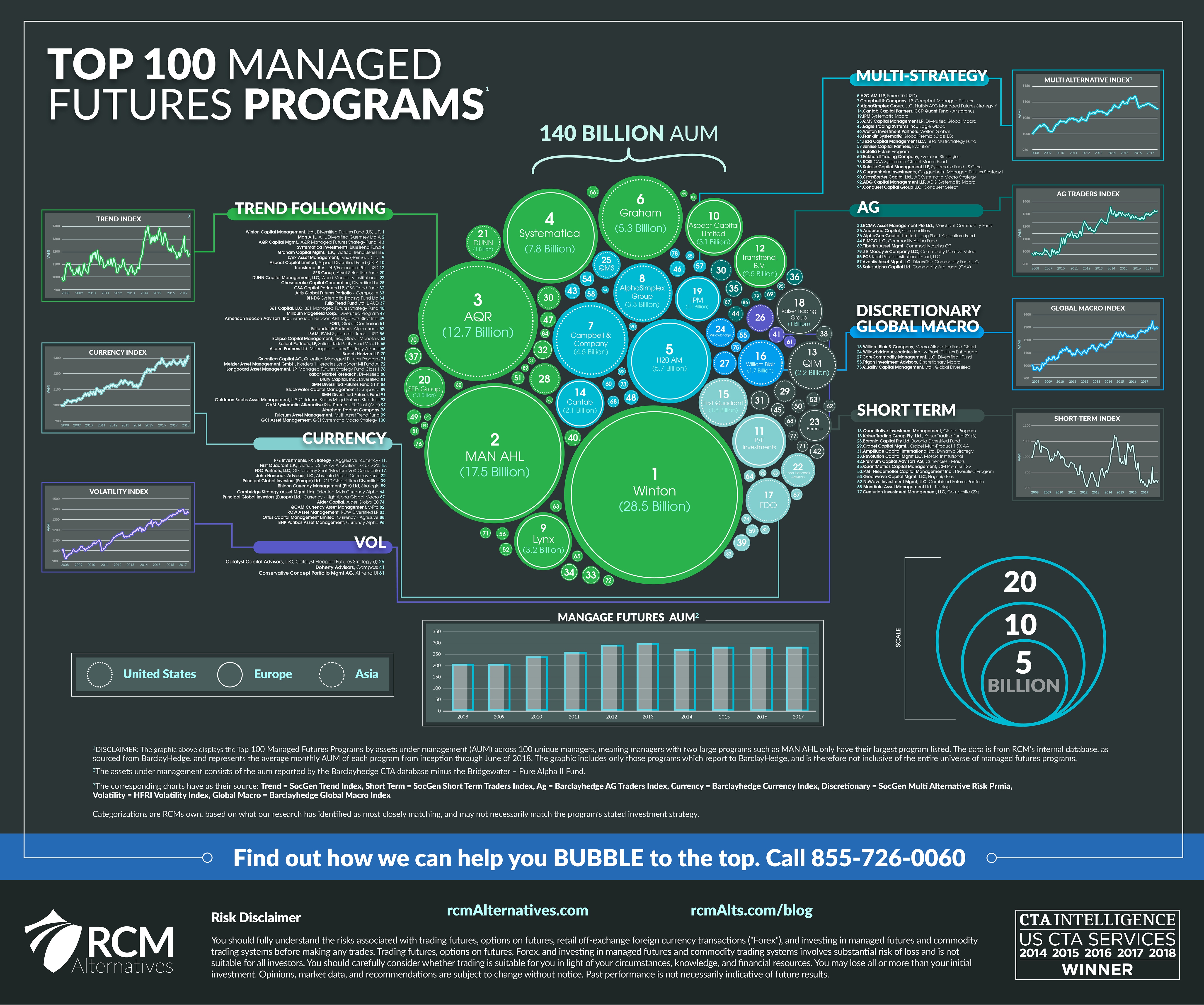

Infographic – Top 100 Managed Futures Programs, RCMAlternatives.com

{kind=link}

Quant Hedge Funds Trail Old-School Ones, But Reap All the

New Money, CIO [pwd wall]

The allure of computer-based investing is powerful, despite

inferior returns. https://www.ai-cio.com/in-focus/market-drilldown/quant-hedge-funds-trail-old-school-ones-reap-new-money/

The importance of volatility of volatility, sr-sv.com

Options-implied volatility of U.S. equity prices is measured

by the volatility index, VIX. Options-implied volatility of volatility is measured

by the volatility-of-volatility index, VVIX. Importantly, these two are

conceptually and empirically different sources of risk. Hence, there should

also be two types of risk premia: one for the uncertainty of volatility and for

the uncertainty of variation in volatility. The latter is often neglected and

may reflect deep uncertainty about the structural robustness of markets to

economic change. A new paper shows the importance of both risk factors for

investment strategies, both theoretically and empirically. For example, implied

volatility and “vol of vol” typically exceed the respective realized

variations, indicating that a risk premium is being paid. Also, high measured

risk premia for volatility and “vol-of-vol” lead to high returns in investment strategies

that are “long” these factors. http://www.sr-sv.com/the-importance-of-volatility-of-volatility/

SOCIETY AND CAPITAL

On Preferring A to B, While Also Preferring B to A, Tim

Taylor

"In the last quarter-century, one of the most

intriguing findings in behavioral science goes under the unlovely name of

`preference reversals between joint and separate evaluations of options.' The

basic idea is that when people evaluate options A and B separately, they prefer

A to B, but when they

evaluate the two jointly, they prefer B to A." Thus,

Cass R. Sunstein begins his interesting and readable paper "On preferring

A to B, while also preferring B to A" (Rationality and Society 2018, first published July 11, 2018, subscription

required). http://conversableeconomist.blogspot.com/2018/07/on-preferring-to-b-while-also.html

Longevity bond pricing in equilibrium, Jevtic et al.

there exists a risk that liabilities related to previous

financial commitments grow higher than expected due to the unreliability of

forecasts of mortality trends. This risk is called longevity risk ;

essentially, it is the risk that lives in a reference population might, on

average, live longer than anticipated. It is clear that providers of pension

plans, annuity, and social insurance share a strong interest in proper

assessment and management of this risk. Whereas assessing longevity risk is

intimately connected with the development of better mortality models with

stronger forecasting capabilities, its management, in order to facilitate

transfer of longevity risk to capital markets, is at least in part dependent on

the development of mortality linked financial instruments, such as mortality

bonds, swaps, and mortality options type derivatives…We consider a model with

stochastic mortality intensity that affects the income of agents in the market

and introduce a longevity bond market that can be used to hedge longevity risk.

By using the Clark-Haussmann formula, we prove that our longevity bond

completes the market. In addition, we provide numerical results for the

survivorship longevity bond. https://ssrn.com/abstract=3206195

How Does Consumption Habit Affect the Household's Demand for

Life-Contingent Claims? Tan et al.

This paper examines the impact of habit formation on demand

for life-contingent claims in a life-cycle model. We solve the optimal

consumption, portfolio choice, and life insurance/annuity problem analytically,

and illustrate the mechanism how consumption habit can alter the bequest motive

and therefore drive the demand for life-contingent products. We show that habit

formation alone can partially address the mismatch in the life insurance market

between the life insurance holdings of most households and their underlying

financial vulnerabilities, or the mismatch in the annuity market between the

lack of any annuitization and the risk of outliving their financial wealth, but

not both. However, habit formation together with social security may shed some

light on the puzzling thinness of both life insurance and voluntary annuity

market. https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3211009

Unambiguous Uncertainty, Sam Savage

So, what’s the difference between these two experiments? In

the second one, the subject’s amygdala (the emotional center of the limbic

system, which triggers the fight or flight response) lights up like a Christmas

tree when viewed with functional MRI! The explanation for this strong reaction

is that the ambiguity of the second deck induces anxiety[1]… The relevance to

probability management is that in our discipline, uncertainty is communicated

in SIPs (Stochastic Information Packets), which are randomly shuffled potential

outcomes similar to the first deck of cards. With SIPs, the uncertainty is

unambiguous. https://www.probabilitymanagement.org/blog/2018/7/24/unambiguous-uncertainty

No comments:

Post a Comment