--------------------

Update 7/23/17: Read this post first. The post below might've been a little too sanguine and the performance since then has only gotten worse. I'm not as optimistic on peer lending as I might have been when I first wrote this up.

--------------------

Earlier this year I posted -- since I have an interest in, and a non-trivial allocation to, a whole slew of alternative risk premia from momentum to peer lending to tactical fixed income to alt international credit to FX to short volatility etc… -- a comment on peer-to-peer lending on LinkedIn. I almost immediately got a comment (that I can no longer retrieve) from a friend from college, a professional financial advisor, that said something like: "beware of peer lending, it's not ready for prime time…I lost X% in my first year." I can't remember but it was more or less -10% or so. That was so different from my own experience that I decided to do a moderately deep dive into my own data. Maybe he was making individual loans or high risk loans or whatever. Me? I have done lower risk, automatically invested, and very, very diversified lending. Maybe it's apples and oranges. Here are five things I see from my vantage point:

Update 7/23/17: Read this post first. The post below might've been a little too sanguine and the performance since then has only gotten worse. I'm not as optimistic on peer lending as I might have been when I first wrote this up.

--------------------

Earlier this year I posted -- since I have an interest in, and a non-trivial allocation to, a whole slew of alternative risk premia from momentum to peer lending to tactical fixed income to alt international credit to FX to short volatility etc… -- a comment on peer-to-peer lending on LinkedIn. I almost immediately got a comment (that I can no longer retrieve) from a friend from college, a professional financial advisor, that said something like: "beware of peer lending, it's not ready for prime time…I lost X% in my first year." I can't remember but it was more or less -10% or so. That was so different from my own experience that I decided to do a moderately deep dive into my own data. Maybe he was making individual loans or high risk loans or whatever. Me? I have done lower risk, automatically invested, and very, very diversified lending. Maybe it's apples and oranges. Here are five things I see from my vantage point:

1. This has been low volatility, consistent, moderate

return stuff.

I started allocating to peer lending sometime in 2009, around seven years ago.

I measured only from 3/2011 (~5 years) since I stopped contributing after

that point which made the spreadsheeting easier since I don’t have to time-weight

the returns. The end date is 4/30/2016 .

I looked at nothing other than the end-of-month account value that Lending Club

(LC; platform of choice) reported to me. That means it is net of defaults and

fees. As mentioned, I pay LC to

automatically invest. I am not choosing loans.

My selected distribution of risk is moderate to low (I'll publish that some other

time). Over that time frame the compound total annual return has been just shy of 7%. This is

what LC looked like compared to: a) the S&P, b) an allocated 40/60 ETF with

dividends, and c) a hypothetical 7% compounded return:

2. The rolling returns show some expected degradation but

they are more stable than I thought.

When one first makes an allocation to loans, there are no

defaults for a while so one feels like a genius for about a year. After that the defaults kick in and the

returns start to suffer. Over a long

enough time frame one can see the defaults in returns and over a very long

timeframe (a timeframe I have not seen) one could maybe even see the effects of

economic cycles among other things. This is what the rolling 12 month returns

of ending account values looks like for me from Q12011 thru Q12016 . As expected, they are high in the beginning and suffer a bit thereafter:

3. The returns in any given month, due to default

experience, seem to vary a bit…more than I thought.

This is a chart of the distribution of monthly returns

(annualized). Returns are

excel-histogram-binned so 7% is really all the stuff between 6-7%. The returns are a simple arithmetic

annualization. The average is just under

7%. There is a positive skew. In practice in any given month, I am often

surprised by how little I get paid and I often under-appreciate when the

payment is more than expected.

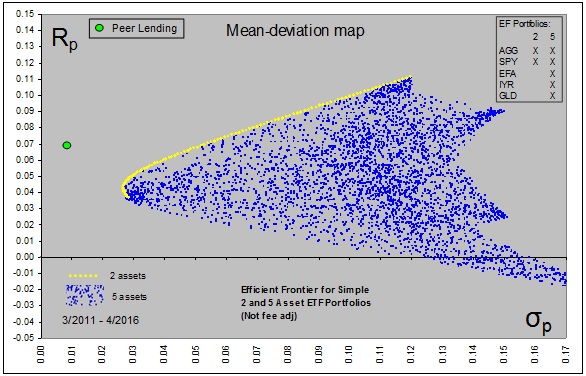

4. The allocation, in isolation, looks like it is accretive

to my efficient frontier as far as I can tell.

Take this chart with a grain of salt. I think I made a few math/modeling errors. Also

there is almost infinite quibbability (I made that word up) over the selection

of comparison ETFs for ex-post analysis. That said, in terms of a general order

of magnitude, I'm guessing that the allocation to LC has been generally

accretive to the (my) efficient frontier.

I use this kind of thing, not so much as science, but rather as a management decision making tool, something like: "should I keep doing

what I'm doing or should I stop."

Answer for now is "keep doing."

Various allocations of AGG SPY EFA IYR and GLD over 2011-2016 compared to LC.

5. The low volatility and moderate returns comes at a

sleep-at-night-risk cost that I can't really quantify.

My best guess is that there are a lot of risks that I have

not really understood in this endeavor.

Here are some random thoughts on what I may be paying for my returns:

- I will likely continue to see declining returns due to

defaults as the portfolio ages. This is

a pretty mature portfolio past the 36 month mark so maybe not but the chances

of holding on to a 7% compound return, or even 6%, over the long run (say 20-30

years?) is not confidence-inspiring.

- I may see declining returns or capital shocks from

external or systemic stuff. Certainly LC has been in the news lately and there

is a lot of chatter about the supply and demand equation of peer lending as

well as the unholy influence of institutional investors. I have no idea how all this is going to play

out.

- I started this in '09.

I, and P2P, have not seen peer lending go through a full economic

cycle. I have to imagine that that will

not be so much fun especially for something that has what I'll call pseudo-liquidity.

- Did I mention liquidity? While it is not exactly a private

placement with a lockup it is also not something I can sell efficiently. I can maybe wait for loans to mature over 1

or 2 or 3+ years or I can try to sell on a sketchy secondary market. I have no illusions that I can walk away

pain-free whenever I wish.

- The recent news about the LC CEO woke me up to the risk

that LC could totally implode. Could I

get my money back if LC goes bankrupt?

The paper from LC tells me so but 58 years of experience also tell me

that contracts mean s*it when bad things happen. It's all smiles, handshakes and backslapping

until the creditors and their lawyers step in.

- There could be a regulatory intrusion. Not to get

political but the current political environment feels a wee bit hostile to

innovation and entrepreneurialism in general and finance/lending in

particular. That is not a good headwind

for FinTech like peer2peer. There is NO

way to predict how that might affect me as an investor except in negative terms.

No comments:

Post a Comment